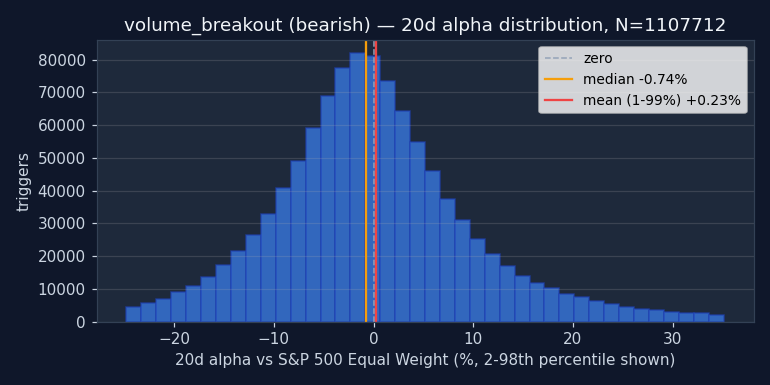

volume_breakout

Volume breakout

Detects unusual volume spikes exceeding N× the rolling average. Bullish: volume spike with close > open (buying pressure). Bearish: volume spike with close < open (selling pressure).

Signal family

Trend — Signals that fire when price is continuing or reversing an established directional move. Momentum-following by nature.

Parameters

| Name | Description | Default | Range |

|---|---|---|---|

| period | Average volume lookback (days) | 20 | 5–100 |

| multiplier | Volume multiplier threshold | 2.0 | 1.5–5.0 |

Historical context

3,067,357 triggers on 24,029 tickers, 1995-09-27 → 2026-05-01. Universe: US large-cap (mcap ≥ $100,000,000, price ≥ $1). Long-only convention: BUY at open T+1, hold the horizon, compare to S&P 500 Equal Weight over the same window.

Methodology footnotes

Benchmarks shown in the detail tables: spxew (S&P 500 Equal Weight — primary, median-stock view, avoids the 2020+ megacap-concentration distortion), spx (S&P 500 cap-weighted, distorted post-2020), msci (MSCI World USD). Per-stock regime tags: trending = ADX(14) ≥ 25, high vol = 20d realized annualized vol ≥ 20%. 1d return = intraday T+1 open→close; 20d = open T+1 to close T+20.

At a glance — alpha vs S&P 500 Equal Weight, US-only

Holding-period sensitivity. Bullish columns: positive = signal worked (long the trigger beat the index). Bearish columns: negative = signal worked (the flagged stock underperformed).

| Horizon | Bullish α | Bearish α |

|---|---|---|

| 5-day | -0.11% | +0.03% |

| 20-day | +0.28% | +0.23% |

| 60-day | +0.83% | +0.54% |

| 1-year | +5.26% | +3.87% |

Sign flip across horizons. Bullish triggers go from -0.11% (5d) to +5.26% (1y) — short-term fade but longer holding recovers and wins.

Bearish: worse than random (p=1.000).

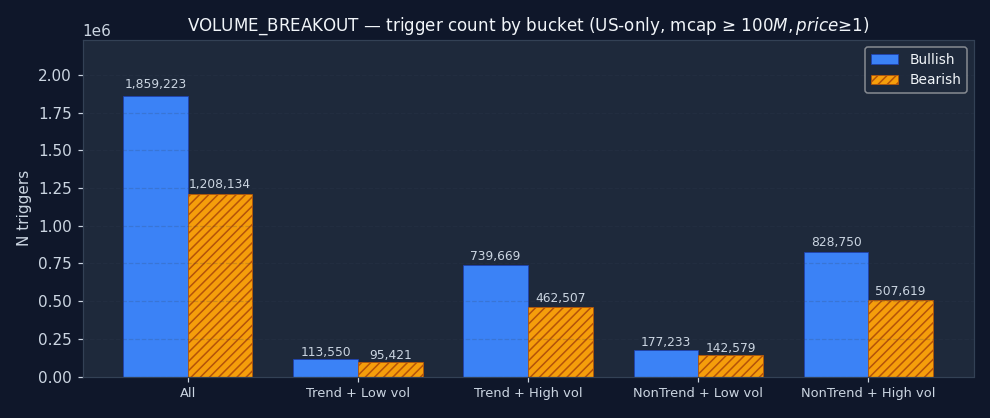

Where does VOLUME_BREAKOUT actually fire?

The bucket distribution often reveals what the signal really is, regardless of its textbook label. Heavy concentration in "non-trending + high vol" = it's mostly a chop-market event. Heavy in "trending + low vol" = it picks up the smooth grinds. Read the chart before the alpha numbers — context shapes everything that follows.

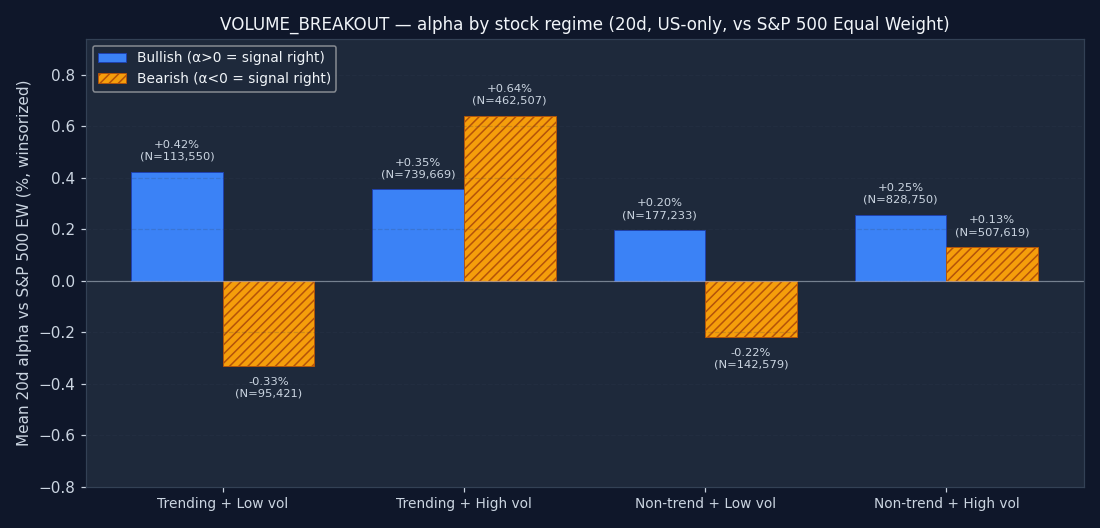

Does it work in every regime?

Trigger alpha split by the host stock's own regime on the trigger date — trending or ranging, high-vol or low-vol. The 20d alpha you'd actually capture if you took the trade. Bars matching your direction's "right" sign (green) = the signal worked in that regime; opposite sign = avoid it there. A signal with one strong-positive bar and three flat ones isn't a "20d alpha" signal — it's a "20d alpha when the stock is X" signal.

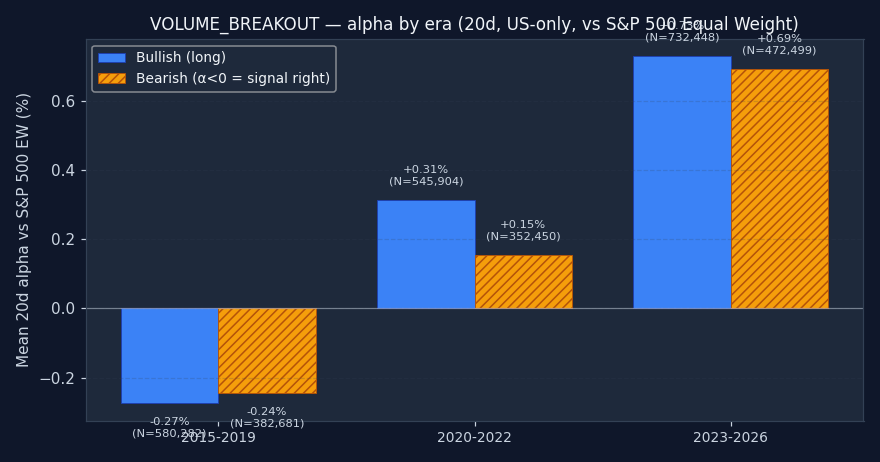

Does it work in every era?

A multi-year average can hide major instability. The sample splits into three windows: 2015–2019 (pre-COVID), 2020–2022 (pandemic + 2022 bear), and 2023+ (post-ZIRP + AI megacap rally). All three matching your direction's "right" sign = the signal is durable. One era doing all the work = a regime-specific edge that may not repeat. The bigger the variance across eras, the smaller the position you should run.

↑ Bullish triggers

| Bench | Metric | 1d | 5d | 20d | 60d | 252d |

|---|---|---|---|---|---|---|

| spx | Stock % | -0.03% | +0.10% | +1.05% | +3.10% | +15.32% |

| Bench % | +0.02% | +0.22% | +1.00% | +3.05% | +13.85% | |

| Alpha % | -0.07% | -0.14% | +0.08% | +0.04% | +1.40% | |

| Median alpha | -0.19% | -0.61% | -1.38% | -3.28% | -10.70% | |

| Hit rate (α>0) | 45.9% | 44.8% | 44.0% | 41.9% | 38.4% | |

| p (naive) | <0.001 | <0.001 | <0.001 | 0.0169 | <0.001 | |

| p (HAC) | <0.001 | <0.001 | <0.001 | 0.2782 | <0.001 | |

| N | 1,793,860 | 1,731,659 | 1,722,001 | 1,689,161 | 1,498,664 | |

| msci | Stock % | -0.03% | +0.10% | +1.05% | +3.10% | +15.32% |

| Bench % | +0.05% | +0.22% | +0.87% | +2.62% | +11.41% | |

| Alpha % | -0.09% | -0.13% | +0.21% | +0.49% | +3.77% | |

| Median alpha | -0.22% | -0.60% | -1.27% | -2.86% | -8.33% | |

| Hit rate (α>0) | 45.3% | 44.7% | 44.5% | 42.8% | 40.8% | |

| p (naive) | <0.001 | <0.001 | <0.001 | <0.001 | <0.001 | |

| p (HAC) | <0.001 | <0.001 | <0.001 | <0.001 | <0.001 | |

| N | 1,783,866 | 1,721,779 | 1,714,095 | 1,677,545 | 1,489,371 | |

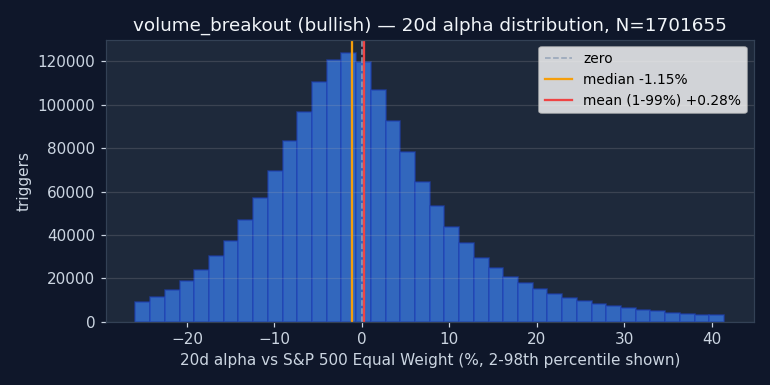

| spxew | Stock % | -0.03% | +0.10% | +1.05% | +3.10% | +15.32% |

| Bench % | +0.04% | +0.20% | +0.81% | +2.28% | +10.16% | |

| Alpha % | -0.08% | -0.11% | +0.28% | +0.83% | +5.26% | |

| Median alpha | -0.20% | -0.57% | -1.15% | -2.45% | -6.70% | |

| Hit rate (α>0) | 45.9% | 45.2% | 45.1% | 43.8% | 42.4% | |

| p (naive) | <0.001 | <0.001 | <0.001 | <0.001 | <0.001 | |

| p (HAC) | <0.001 | <0.001 | <0.001 | <0.001 | <0.001 | |

| N | 1,778,965 | 1,709,651 | 1,701,655 | 1,667,356 | 1,478,228 |

Permutation null detail — all horizons × both benchmarks

| Horizon | Bench | Observed lift | Null mean | Null 95% CI | pperm |

|---|---|---|---|---|---|

| 1d | spx | +0.09% | +0.10% | [+0.10%, +0.11%] | 1.000 |

| 1d | msci | +0.10% | +0.11% | [+0.10%, +0.11%] | 1.000 |

| 1d | spxew | +0.09% | +0.10% | [+0.09%, +0.10%] | 0.955 |

| 5d | spx | +0.38% | +0.44% | [+0.43%, +0.45%] | 1.000 |

| 5d | msci | +0.39% | +0.45% | [+0.44%, +0.45%] | 1.000 |

| 5d | spxew | +0.37% | +0.43% | [+0.42%, +0.44%] | 1.000 |

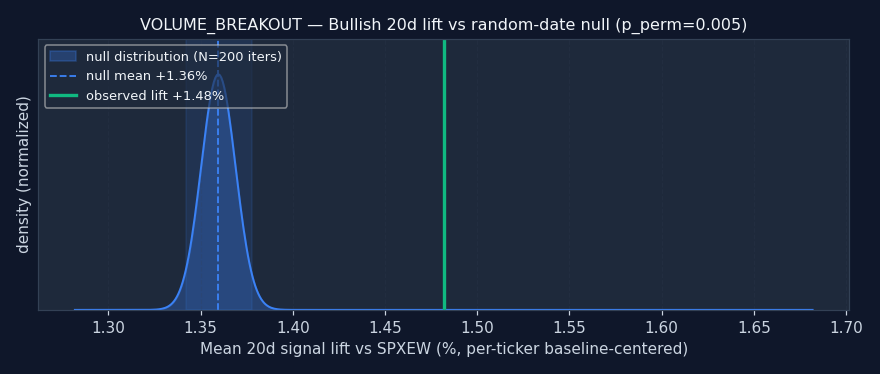

| 20d | spx | +1.51% | +1.39% | [+1.37%, +1.40%] | 0.005 |

| 20d | msci | +1.52% | +1.40% | [+1.38%, +1.42%] | 0.005 |

| 20d | spxew | +1.48% | +1.36% | [+1.34%, +1.38%] | 0.005 |

| 60d | spx | +2.87% | +2.93% | [+2.91%, +2.97%] | 1.000 |

| 60d | msci | +2.90% | +2.95% | [+2.93%, +2.99%] | 1.000 |

| 60d | spxew | +2.91% | +2.88% | [+2.85%, +2.91%] | 0.020 |

| 252d | spx | +5.85% | +5.42% | [+5.33%, +5.50%] | 0.005 |

| 252d | msci | +5.86% | +5.34% | [+5.25%, +5.42%] | 0.005 |

| 252d | spxew | +5.54% | +5.05% | [+4.96%, +5.13%] | 0.005 |

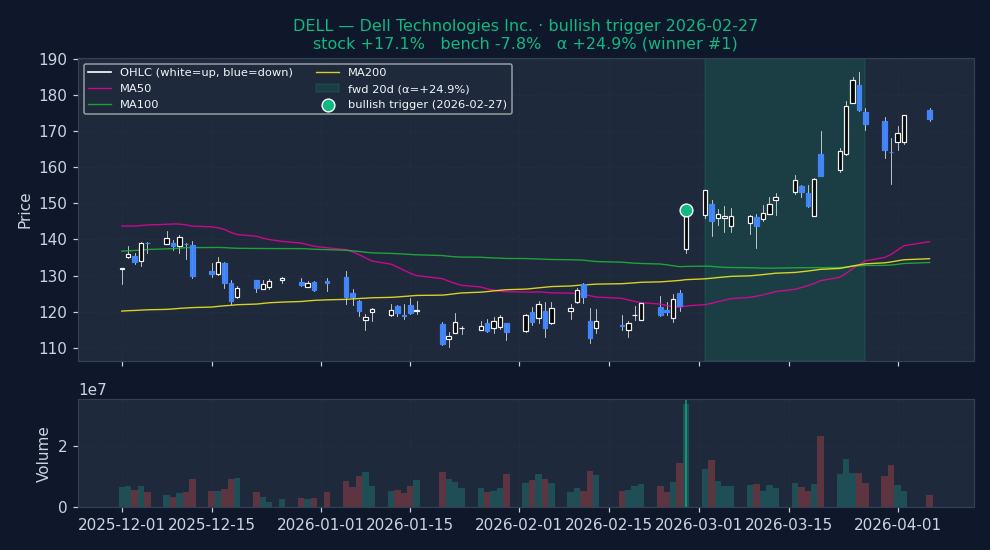

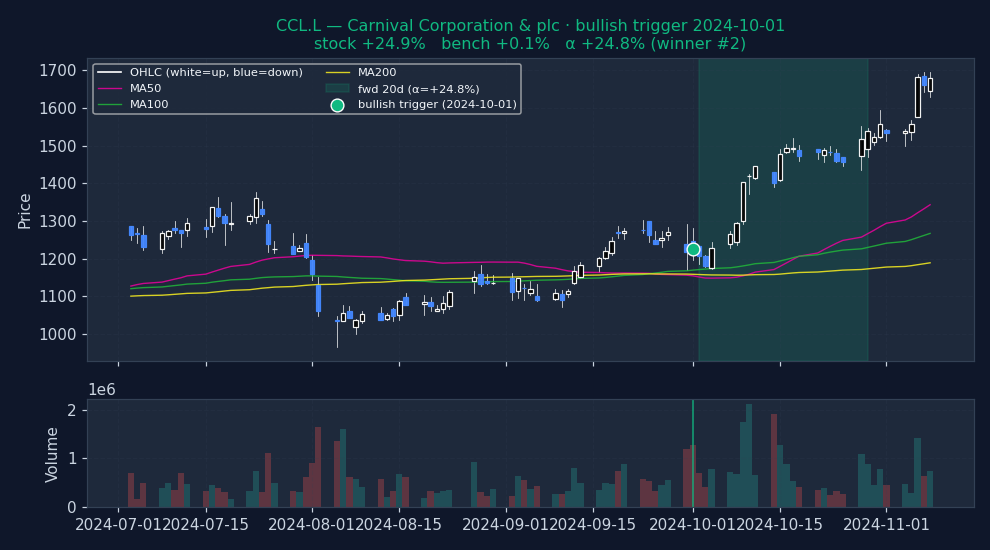

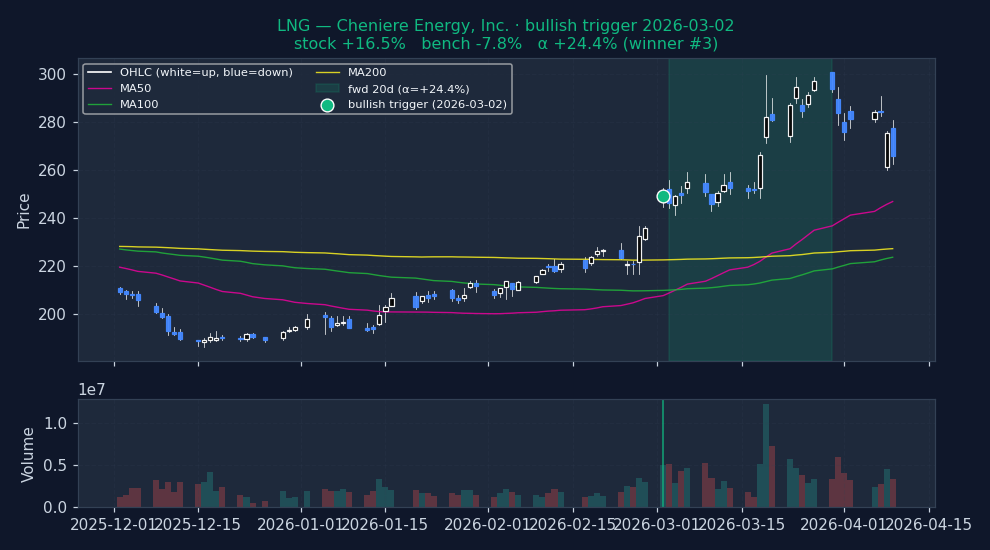

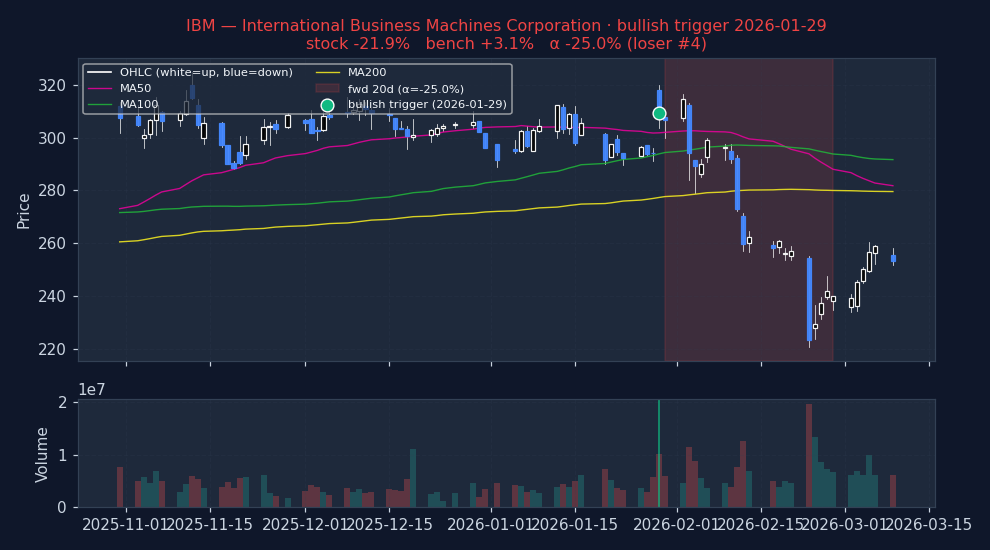

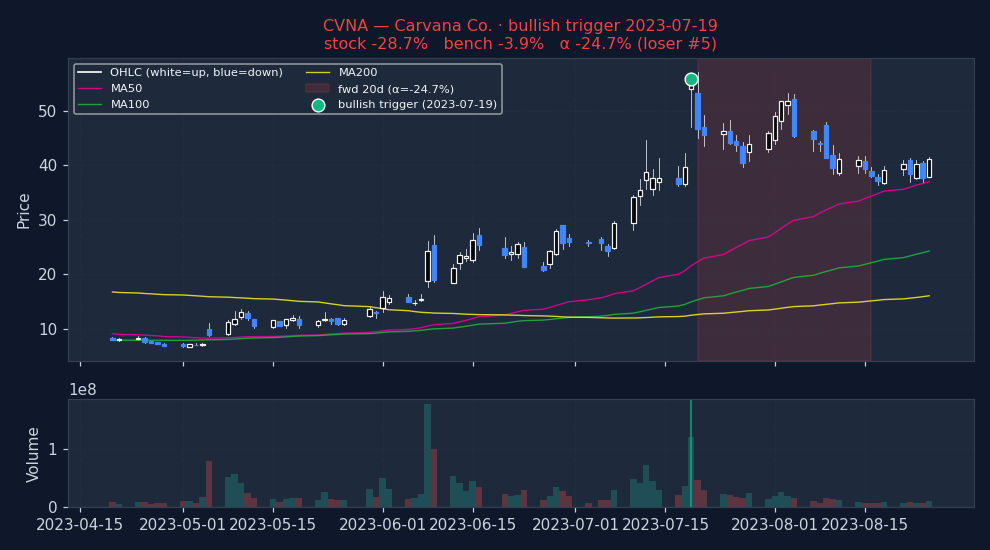

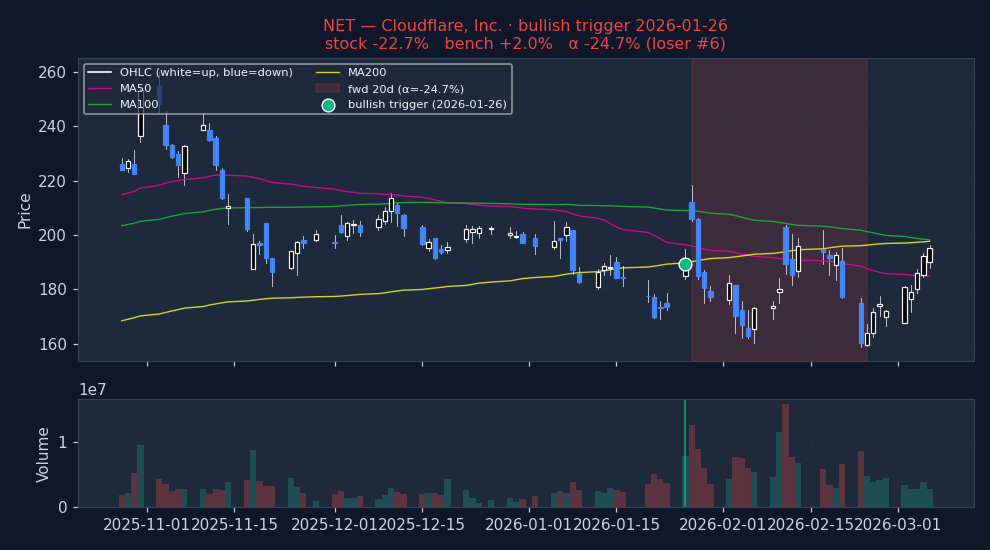

Example triggers on US large-caps (2023+, mcap ≥ $30B)

Six recent bullish VOLUME_BREAKOUT triggers on US mega-caps. Top three: the signal's best outcomes. Bottom three: the worst. Catalyst-driven outliers (|α| > 25%) excluded so what's left is the signal's own typical good and bad days, not earnings shocks.

Strongest outcomes (what VOLUME_BREAKOUT looks like when it works)

Weakest outcomes (what VOLUME_BREAKOUT looks like when it fails)

Stock-regime quadrants (2×2 per-stock, 20d alpha detail table)

| Quadrant | N | Stock % (spx) | Bench % (spx) | Alpha % (spx) | p (HAC) | Stock % (msci) | Bench % (msci) | Alpha % (msci) | p (HAC) | Stock % (spxew) | Bench % (spxew) | Alpha % (spxew) | p (HAC) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Trending + Low vol Clean directional grind, low whipsaw | 113,550 | +0.88% | +0.78% | +0.12% | 0.0003 | +0.88% | +0.63% | +0.28% | <0.001 | +0.88% | +0.50% | +0.42% | <0.001 |

| Trending + High vol Crisis selloff or parabolic rally | 739,669 | +1.15% | +1.03% | +0.13% | <0.001 | +1.15% | +0.88% | +0.27% | <0.001 | +1.15% | +0.82% | +0.35% | <0.001 |

| Non-trending + Low vol Quiet chop, summer doldrums | 177,233 | +0.75% | +0.80% | -0.04% | 0.0649 | +0.75% | +0.67% | +0.10% | <0.001 | +0.75% | +0.57% | +0.20% | <0.001 |

| Non-trending + High vol Classical "whipsaw zone" for momentum | 828,750 | +1.10% | +1.04% | +0.09% | 0.0001 | +1.10% | +0.94% | +0.19% | <0.001 | +1.10% | +0.89% | +0.25% | <0.001 |

Sub-period breakdown table (20d alpha)

| Period | N | Alpha % (spx) | p (HAC) | Alpha % (msci) | p (HAC) | Alpha % (spxew) | p (HAC) |

|---|---|---|---|---|---|---|---|

| 2015-2019 2015-01-01 → 2020-01-01 | 580,282 | -0.47% | <0.001 | -0.27% | <0.001 | -0.27% | <0.001 |

| 2020-2022 2020-01-01 → 2023-01-01 | 545,904 | +0.51% | <0.001 | +0.64% | <0.001 | +0.31% | <0.001 |

| 2023-2026 2023-01-01 → 2099-01-01 | 732,448 | +0.22% | <0.001 | +0.28% | <0.001 | +0.73% | <0.001 |

↓ Bearish triggers negative alpha = signal was right (stock underperformed market)

| Bench | Metric | 1d | 5d | 20d | 60d | 252d |

|---|---|---|---|---|---|---|

| spx | Stock % | +0.01% | +0.19% | +1.11% | +3.16% | +14.38% |

| Bench % | +0.01% | +0.21% | +1.13% | +3.39% | +14.41% | |

| Alpha % | -0.01% | -0.02% | -0.01% | -0.21% | -0.04% | |

| Median alpha | -0.08% | -0.31% | -0.99% | -2.56% | -10.01% | |

| Hit rate (α>0) | 48.1% | 46.9% | 45.1% | 43.0% | 38.4% | |

| p (naive) | 0.0003 | 0.0037 | 0.2951 | <0.001 | 0.4285 | |

| p (HAC) | 0.0003 | 0.0100 | 0.4374 | <0.001 | 0.7784 | |

| N | 1,168,053 | 1,131,719 | 1,122,261 | 1,098,698 | 994,241 | |

| msci | Stock % | +0.01% | +0.19% | +1.11% | +3.16% | +14.38% |

| Bench % | +0.04% | +0.21% | +0.99% | +2.98% | +12.03% | |

| Alpha % | -0.02% | -0.00% | +0.11% | +0.24% | +2.16% | |

| Median alpha | -0.10% | -0.30% | -0.87% | -2.13% | -7.72% | |

| Hit rate (α>0) | 47.7% | 47.0% | 45.6% | 44.0% | 40.8% | |

| p (naive) | <0.001 | 0.6769 | <0.001 | <0.001 | <0.001 | |

| p (HAC) | <0.001 | 0.7116 | <0.001 | <0.001 | <0.001 | |

| N | 1,162,188 | 1,126,052 | 1,114,873 | 1,092,867 | 987,174 | |

| spxew | Stock % | +0.01% | +0.19% | +1.11% | +3.16% | +14.38% |

| Bench % | +0.04% | +0.16% | +0.85% | +2.61% | +10.58% | |

| Alpha % | -0.02% | +0.03% | +0.23% | +0.54% | +3.87% | |

| Median alpha | -0.09% | -0.27% | -0.74% | -1.76% | -6.01% | |

| Hit rate (α>0) | 48.0% | 47.4% | 46.3% | 45.0% | 42.6% | |

| p (naive) | <0.001 | <0.001 | <0.001 | <0.001 | <0.001 | |

| p (HAC) | <0.001 | <0.001 | <0.001 | <0.001 | <0.001 | |

| N | 1,156,821 | 1,116,747 | 1,107,712 | 1,082,836 | 979,077 |

Permutation null detail — all horizons × both benchmarks

| Horizon | Bench | Observed lift | Null mean | Null 95% CI | pperm |

|---|---|---|---|---|---|

| 1d | spx | +0.12% | +0.09% | [+0.08%, +0.09%] | 1.000 |

| 1d | msci | +0.14% | +0.09% | [+0.09%, +0.10%] | 1.000 |

| 1d | spxew | +0.12% | +0.08% | [+0.07%, +0.08%] | 1.000 |

| 5d | spx | +0.44% | +0.37% | [+0.36%, +0.39%] | 1.000 |

| 5d | msci | +0.45% | +0.38% | [+0.36%, +0.39%] | 1.000 |

| 5d | spxew | +0.45% | +0.36% | [+0.35%, +0.37%] | 1.000 |

| 20d | spx | +1.34% | +1.19% | [+1.16%, +1.21%] | 1.000 |

| 20d | msci | +1.34% | +1.19% | [+1.17%, +1.22%] | 1.000 |

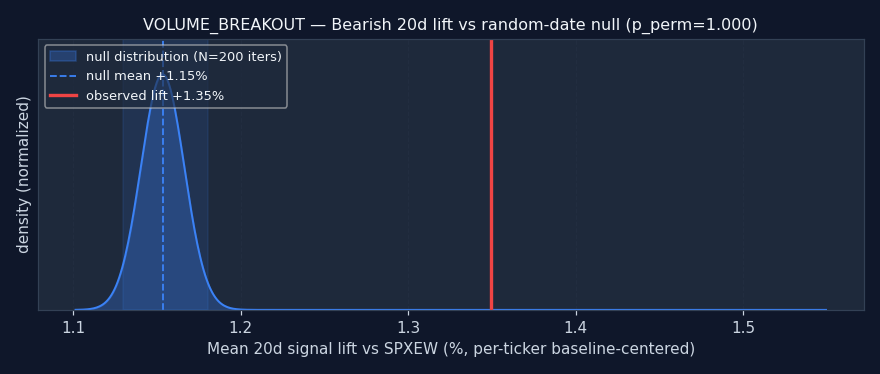

| 20d | spxew | +1.35% | +1.15% | [+1.13%, +1.18%] | 1.000 |

| 60d | spx | +2.74% | +2.52% | [+2.48%, +2.56%] | 1.000 |

| 60d | msci | +2.76% | +2.52% | [+2.49%, +2.57%] | 1.000 |

| 60d | spxew | +2.75% | +2.45% | [+2.42%, +2.49%] | 1.000 |

| 252d | spx | +6.14% | +5.12% | [+5.06%, +5.19%] | 1.000 |

| 252d | msci | +6.02% | +5.05% | [+4.99%, +5.13%] | 1.000 |

| 252d | spxew | +5.93% | +4.76% | [+4.70%, +4.84%] | 1.000 |

Example triggers on US large-caps (2023+, mcap ≥ $30B)

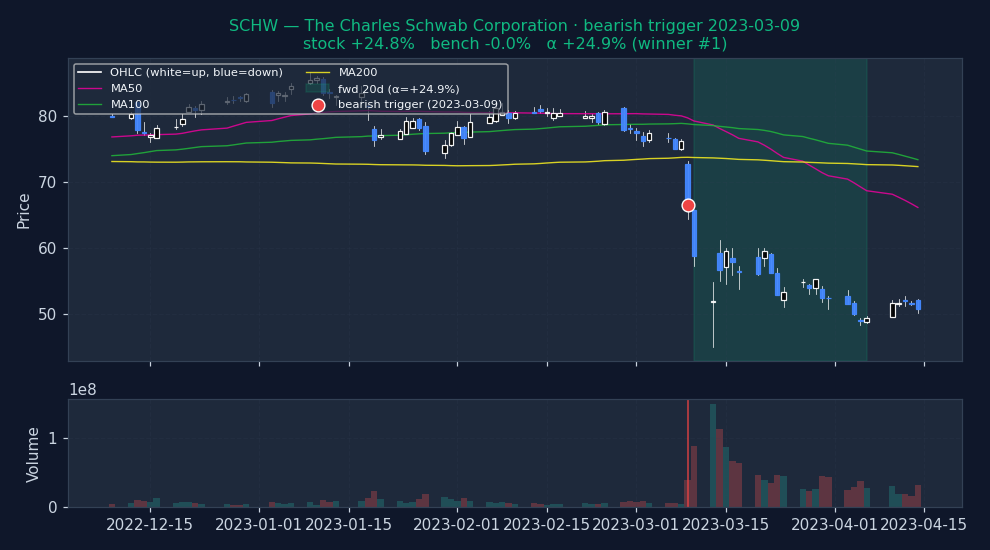

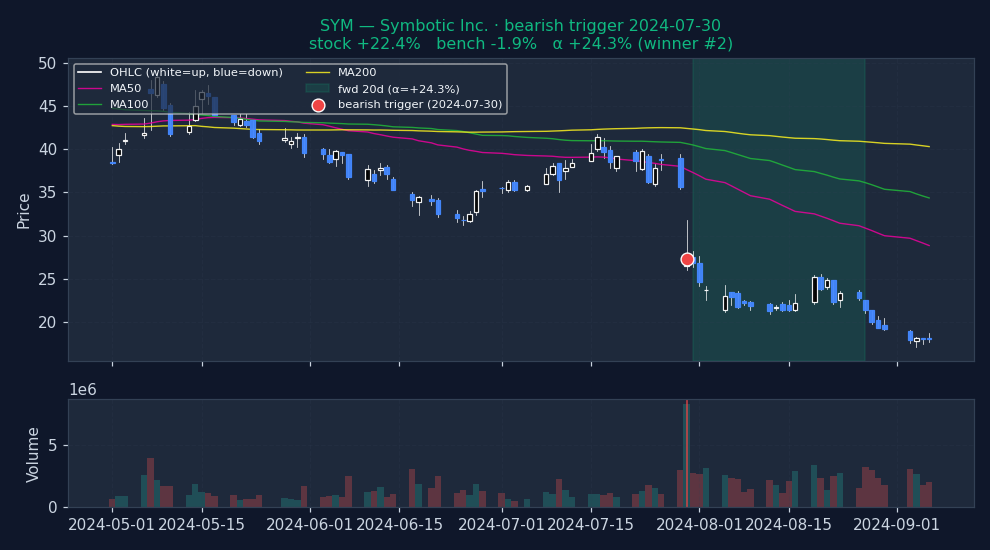

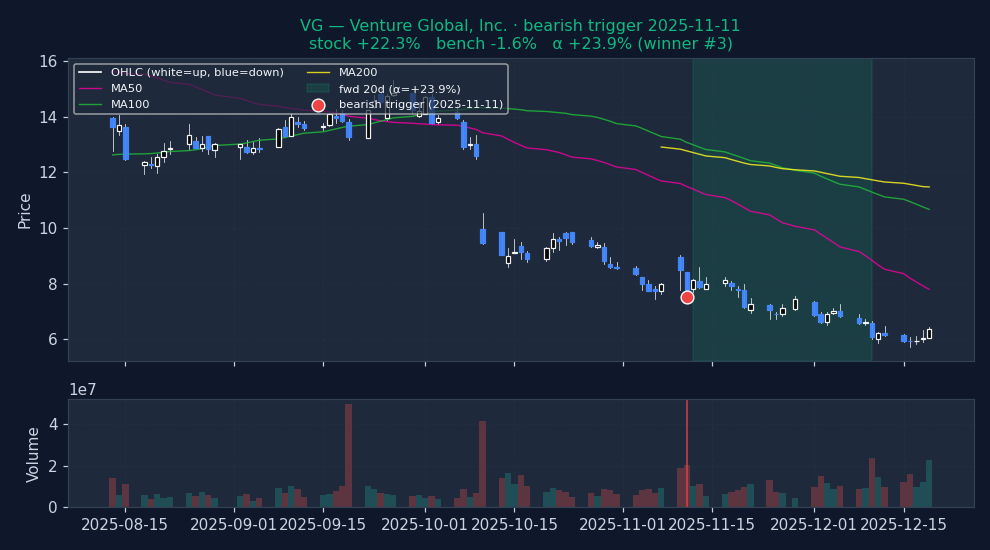

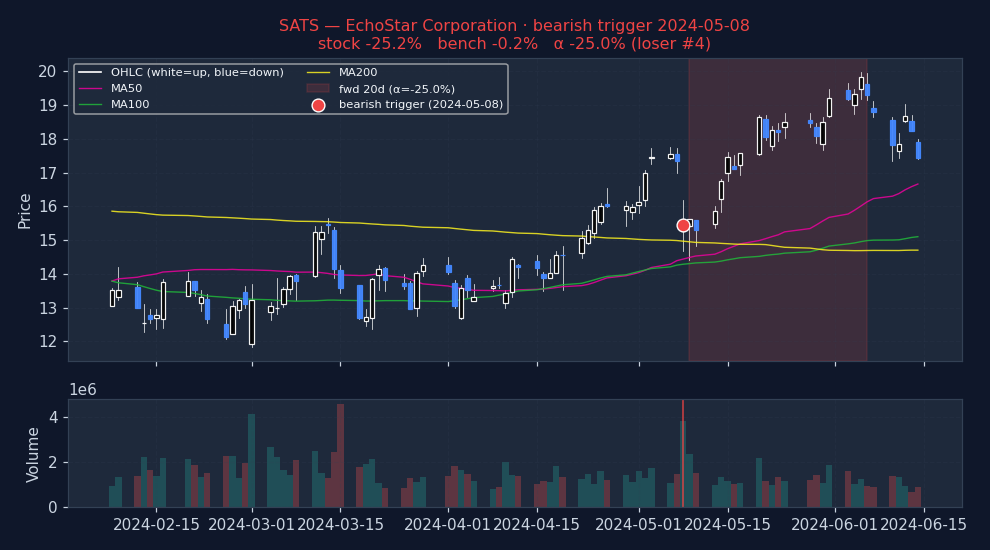

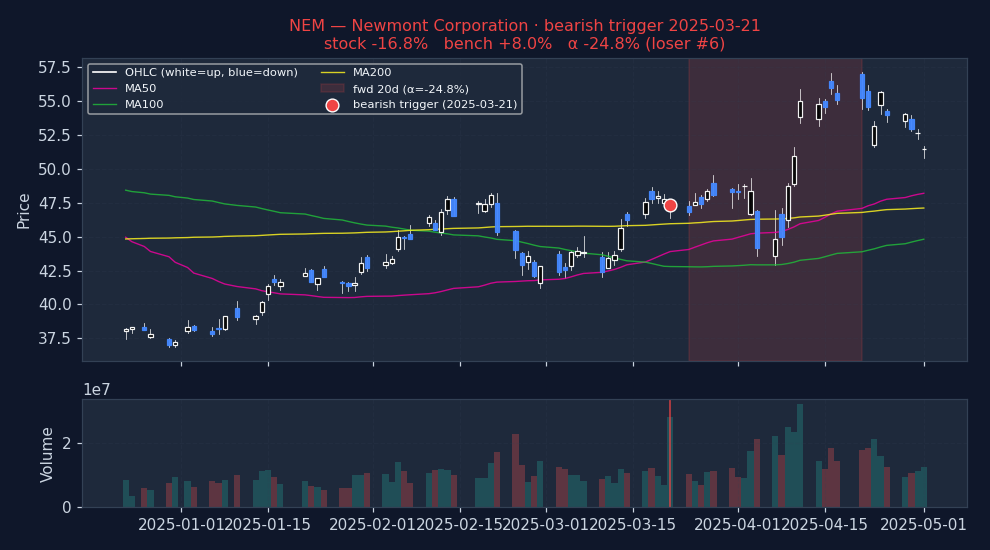

Six recent bearish VOLUME_BREAKOUT triggers on US mega-caps. Top three: the signal's best outcomes. Bottom three: the worst. Catalyst-driven outliers (|α| > 25%) excluded so what's left is the signal's own typical good and bad days, not earnings shocks.

Strongest outcomes (what VOLUME_BREAKOUT looks like when it works)

Weakest outcomes (what VOLUME_BREAKOUT looks like when it fails)

Stock-regime quadrants (2×2 per-stock, 20d alpha detail table)

| Quadrant | N | Stock % (spx) | Bench % (spx) | Alpha % (spx) | p (HAC) | Stock % (msci) | Bench % (msci) | Alpha % (msci) | p (HAC) | Stock % (spxew) | Bench % (spxew) | Alpha % (spxew) | p (HAC) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Trending + Low vol Clean directional grind, low whipsaw | 95,421 | +0.26% | +0.89% | -0.64% | <0.001 | +0.26% | +0.71% | -0.46% | <0.001 | +0.26% | +0.57% | -0.33% | <0.001 |

| Trending + High vol Crisis selloff or parabolic rally | 462,507 | +1.61% | +1.26% | +0.36% | <0.001 | +1.61% | +1.07% | +0.50% | <0.001 | +1.61% | +0.94% | +0.64% | <0.001 |

| Non-trending + Low vol Quiet chop, summer doldrums | 142,579 | +0.40% | +0.89% | -0.47% | <0.001 | +0.40% | +0.75% | -0.32% | <0.001 | +0.40% | +0.67% | -0.22% | <0.001 |

| Non-trending + High vol Classical "whipsaw zone" for momentum | 507,619 | +1.06% | +1.16% | -0.07% | 0.0016 | +1.06% | +1.03% | +0.02% | 0.3513 | +1.06% | +0.92% | +0.13% | <0.001 |

Sub-period breakdown table (20d alpha)

| Period | N | Alpha % (spx) | p (HAC) | Alpha % (msci) | p (HAC) | Alpha % (spxew) | p (HAC) |

|---|---|---|---|---|---|---|---|

| 2015-2019 2015-01-01 → 2020-01-01 | 382,681 | -0.38% | <0.001 | -0.15% | <0.001 | -0.24% | <0.001 |

| 2020-2022 2020-01-01 → 2023-01-01 | 352,450 | +0.20% | <0.001 | +0.34% | <0.001 | +0.15% | <0.001 |

| 2023-2026 2023-01-01 → 2099-01-01 | 472,499 | +0.15% | <0.001 | +0.15% | <0.001 | +0.69% | <0.001 |

Methodology and caveats

How to read. Entry at open of T+1 (one trading day after the signal fires on close of T). 20d = open T+1 to close T+20. Alpha = stock return − benchmark return over the same window (Convention A, single-sided, textbook). For bullish triggers, POSITIVE alpha = signal was right. For bearish triggers, NEGATIVE alpha = signal was right (stock underperformed market). No sign-flipping; the direction of the bet determines what "good" looks like. Per-stock regime is each stock's own ADX(14) and RV(20) at the trigger date — not market-wide state.

Three p-values, three robustness tests. (a) p_naive: scipy one-sample t-test on winsorized alphas. Optimistic because overlapping 20d windows on the same ticker inflate effective N. (b) p_hac: Newey-West HAC with lag = horizon — corrects for the overlap and is the academic-finance standard. (c) p_perm: fraction of 200 random-date null iterations with mean ≥ observed. Tests whether the signal beats random date selection at all. A signal that clears all three (pnaive, phac, pperm all < 0.05) has real information; a signal that fails pperm has zero edge even if the t-test says "significant."

Caveats. (i) Universe reflects today's active tickers; delisted losers pruned → survivorship bias. (ii) Mcap ≥ $100M filter uses today's snapshot, not point-in-time — mild lookahead on which stocks enter the sample, not on returns. (iii) Means and p-values use winsorized alphas (1/99 percentile) to prevent data errors from dominating. Medians and hit rates use raw data. (iv) Zero transaction costs assumed. Realistic bid-ask + commissions remove 20–40bps from 20d alpha on US large-caps, more on small-cap. Sub-20bps alpha is noise in practice. (v) Past performance does not predict future results.

How to use this

1 · When to reach for this signal

Use Volume breakout bullish as a long-side screening tile. Observed 20d alpha vs S&P 500 Equal Weight is +0.08%, which beats random (permutation test, 200 iterations). The bearish side does not add edge (worse than random ) — treat it as noise, not a short trigger.

2 · When it works — the setups that drive it

- Best bullish setup: Trending + High vol — alpha +0.13% / 20d on 739,669 historical triggers.

- Best bearish setup: Trending + High vol — alpha +0.36% / 20d on 462,507 historical triggers.

- Best era for bullish: 2020-2022 — alpha +0.51% / 20d.

- Best era for bearish: 2020-2022 — alpha +0.20% / 20d.

3 · When it fails — common false positives

- Weakest bullish cell: Non-trending + Low vol — alpha -0.04% / 20d on 177,233 triggers.

- Weakest bearish cell: Trending + Low vol — alpha -0.64% / 20d on 95,421 triggers.

- Worst era for bullish: 2015-2019 — alpha -0.47% / 20d.

- Worst era for bearish: 2015-2019 — alpha -0.38% / 20d.

Signal-specific failure patterns

4 · Pairing inside a screen

The statements below describe how this signal relates to others by construction — which indicator family it belongs to, and where same-family redundancy might reduce the independence of evidence inside a Daily Report. These are taxonomic classifications drawn from standard technical-analysis texts; they are not pairing backtests. A multi-signal convergence backtest is planned but not yet run.

Complementary to price signals

Volume confirmation is a complementary principle to price signals, not a same-family redundancy. A price breakout or breakdown accompanied by above-average volume carries more weight in classical technical analysis than the same price move on thin volume (Murphy, Technical Analysis of the Financial Markets, 1999; Kirkpatrick & Dahlquist, Technical Analysis, 3rd ed. 2015). Combining volume_breakout with any price-based signal in the same direction adds weight rather than redundant evidence.

What would likely rescue this signal

This block calls out the data or conditions that could turn a technically weak signal into a usable one in a composite screen. Based on signal mechanics and the observed failure patterns above; individual combinations are not yet backtested.

- Combine with price-level breakouts — Volume-confirmed breakouts are the textbook institutional accumulation signature. Pairing with new 20d or 52w highs would filter for real technical events rather than random volume spikes. This is the most natural rescue path.

- Multi-day volume pattern — Signal is currently a single-day volume event. A 3-day sustained volume pattern (each day > 1.5× average) would reduce noise and might reveal cleaner alpha. Parameter tuning opportunity.

See also Why technical-only signals don't survive on their own for the broader argument.

5 · Before you act — a 5-point checklist

- Normal trading day? Rule out earnings (within ±3 days), ex-dividend, or known corporate-action dates — the signal is almost certainly reading noise, not momentum, in those windows.

- Where is price vs its own 50 / 200 DMA? A trend signal is only as credible as the underlying trend it claims to confirm. Check the 200DMA orientation before acting.

- What's the sector breadth doing? An isolated signal in a broadly down-trending sector is a lower-confidence setup than one firing with the rest of its peer group.

- Is ADV20 enough for your size? If the trigger is on a $500M name and you want to move $1M notional, you're the tape. Consider adv20d ≥ 5% of your intended position.

- What invalidates you? Define a price level (for longs: a close below the trigger-day low; for shorts: close above the trigger-day high) and honor it. The backtest alpha is an average; any one trade can be at either tail.

Execution notes

Neither direction has strongly tradable alpha on its own under Convention A. The 2023+ bullish sub-period is intriguing but one sub-period is not conclusive. Best use: as a confirmation filter layered onto a structural breakout trigger (new_20d_high, new_52w_high). Entry open T+1.